Bifurcation in the Gold Market

Why North American investors are selling gold while Chinese investors keep buying

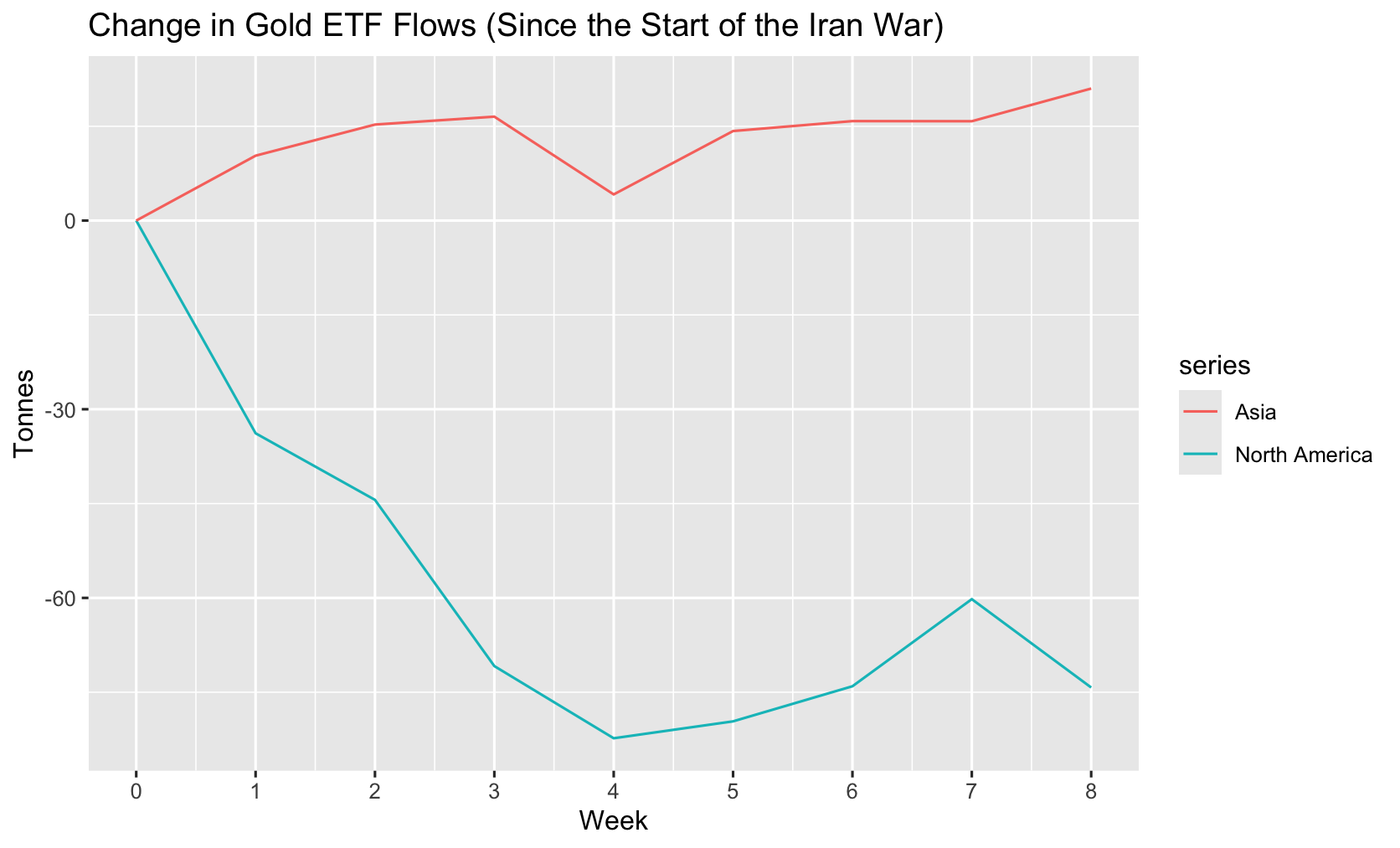

In our last newsletter (Why Is Gold Down During a War?), we looked at why the gold price dropped after the Iran war started. That story turns out to be incomplete. The fall in demand isn’t universal — it’s driven almost entirely by selling in the United States. Chinese demand has actually accelerated. Below we walk through why North American and Chinese investors are pulling in opposite directions.

Why U.S. demand fell

There are two reasons. The first is straightforward: when the war began, the dollar caught a flight-to-safety bid. A stronger dollar mechanically pressures the gold price. The second is real yields. Nominal Treasury yields rose more than inflation expectations after the war began, which means real yields rose — and gold, which pays no income, loses to bonds when real yields climb. That’s the textbook reason gold falls in this kind of environment.

Why Chinese demand didn’t follow

If this logic applied everywhere, Chinese investors would have sold too. They didn’t. They bought. There are two distinct reasons, and it’s worth separating them.

The first is fiscal. U.S. federal debt just crossed $40 trillion and surpassed 100% of GDP. There are only three ways out of a debt load that large: grow out of it, default, or inflate it away. Growth alone won’t get there. Default is politically impossible for the world’s reserve currency. That leaves inflation. For a Chinese investor weighing dollar assets, this isn’t a tail risk — it’s the most likely outcome over a multi-decade horizon. Gold, which has no issuer and no counterparty, doesn’t carry this risk.

The second is geopolitical. When Russia invaded Ukraine in 2022, the U.S. and EU froze roughly $300 billion of Russian central bank reserves held in Western financial institutions. Private Russian assets followed — yachts seized, London real estate frozen. For Chinese investors, especially anyone thinking about a Taiwan scenario, that changed the math. Dollar assets aren’t only subject to inflation risk; they’re subject to political risk. American citizens don’t carry that risk on their domestic holdings. Chinese citizens do. Gold sitting in a Shanghai vault has neither problem.

These two reasons reinforce each other, but they’re independent. Even if U.S. debt sustainability improved tomorrow, the seizure risk would remain. And the shift predates the Iran war — Chinese central bank gold buying has been running at record levels since 2022. The war is accelerating an existing reallocation, not creating one.

There’s also a cultural piece. Gold’s share of household wealth is much higher in China and India than in the U.S. — a generational preference for physical, non-financial savings that doesn’t disappear when real yields in New York move 50 basis points. Combine that household-level demand with the institutional shift in central bank buying, and you get a source of demand that doesn’t behave the way Western markets expect.

What to watch

Two indicators worth tracking month to month:

- North American gold ETF flows. Published monthly by the World Gold Council. The Western retail and institutional signal.

- The Shanghai–London gold premium. When Chinese physical demand exceeds what the international system supplies at the global price, the premium widens. Historically near zero, it’s been sitting $30–50 above London for most of the past year.

If the Shanghai premium compresses and Western ETF flows return, the bifurcation is fading. If both stay where they are, this is a structural shift, and the next leg of gold’s price depends on Asia, not New York.

This article is for informational and educational purposes only and does not constitute financial advice. The author is not a licensed financial advisor. Always do your own research before making investment decisions.